CBSE Accountancy Chapter 3 Recording of Transactions-I class 11 Notes Accountancy in PDF are available for free download in myCBSEguide mobile app. The best app for CBSE students now provides Recording of Transactions-I class 11 Notes Accountancy latest chapter wise notes for quick preparation of CBSE exams and school based annual examinations. Class 11 Accountancy notes on Chapter 3 Recording of Transactions-I class 11 Notes Accountancy are also available for download in CBSE Guide website.

CBSE Guide Recording of Transactions-I class 11 Notes

CBSE guide notes are the comprehensive notes which covers the latest syllabus of CBSE and NCERT. It includes all the topics given in NCERT class 11 Accountancy text book. Users can download CBSE guide quick revision notes from myCBSEguide mobile app and my CBSE guide website.

Recording of Transactions-I class 11 Notes Accountancy

Download CBSE class 11th revision notes for Chapter 3 Recording of Transactions-I class 11 Notes Accountancy in PDF format for free. Download revision notes for Recording of Transactions-I class 11 Notes Accountancy and score high in exams. These are the Recording of Transactions-I class 11 Notes Accountancy prepared by team of expert teachers. The revision notes help you revise the whole chapter in minutes. Revising notes in exam days is on of the best tips recommended by teachers during exam days.

Download Revision Notes as PDF

CHAPTER – 3

Recording of Transactions-I class 11 Notes Accountancy

LEARNING OBJECTIVES

After studying this chapter, you will be able to:

· Explain how to prepare accounting Vouchers.

· Apply accounting equation to explain the effect of transactions.

· Record transactions using rules of debit and credit.

· Record transactions in journal and other subsidiary books.

Suggested Method: Discussion Method, Illustration method, problem solving method etc.

ACCOUNTING EQUATION

An Accounting equation is based on the dual concept of accounting, according to which, every transaction has two aspects namely Debit and Credit. It means that every transaction in accounting effect both Debit (DR.) and Credit (Cr.) side equally.

Total assets of the business firm are financed through the funds raised from either the outsiders (which consists generally Creditors and lenders) or the Owners (which is called Capital).

According to Business entity concept, Business is separate legal entity from its owner thus the amount invested by the owner in the business is liability of the business is called Captial. Accounting equation thus referred to a equation in which total assets is always equal to total Liabilities (i.e. Capital + Liabilities)

Assets = Capital + Liabilities

ANALYSIS OF BUSINESS TRANSACTIONS

Business transaction may affect either both sides of the equation or one side of the equation but the ultimate effect must be equal on the both sides. All the effects are as follows:-

1. Transaction affecting both sides of the equation: A. Commenced business with Cash Rs. 3,00,000.

| Assets | = | Capital + Liabilities | ||

| Cash | Capital | |||

| Transactions | 3,00,000 | = | 3,00,000 | |

Explanation:- As Cash is invested by the owner, it should be shown in Capital (anything which is bring in by the owner is termed as Capital) & Business is receiving asset in the form of cash, it is to be shown in the Assets side as Cash.

B. Bought goods from Ram Rs. 30,000

Effect

| Assets | = | Capital + Liabilities | ||

| Cash Goods | Capital Creditors | |||

| Old Equation | 3,00,000 + – | = | 3,00,000 + – | |

| Transactions | 0 + 30,000 | = | 0 + 30,000 | |

| N.E. | 3,00,000 + 30,000 | = | 3,00,000 + 30,000 | |

Explanation:- As goods is purchased on credit, one effect is that it should be shown in the assets side as Goods & other effect is that goods are purchased on credit so it is to be shown in Liabilities as Creditors..

C. Sold goods (costing Rs. 10000) for cash at Rs. 13000 Effect

| Assets | = | Capital + Liabilities | ||

| Cash Goods | Capital Creditors | |||

| Old Equation | 3,00,000 + 30,000 | = | 3,00,000 + 30,000 | |

| Transactions | +13000 + 10,000 | = | + 3000 + 30,000 | |

| N.E. | 3,13,000 + 20,000 | = | 3,03,000 + 30,000 | |

Explanation:- The transaction will affect both sides as cash has been received so it is to be added back in cash (Rs 13,000) & Goods are to be reduced by 10,000 as goods has been sold also profit of Rs. 3,000 Is to be added back in Capital. Net effect will remain same for both sides

D. Paid to creditors Rs. 20,000

| Assets | = | Capital + Liabilities | ||

| Cash Goods | Capital Creditors | |||

| Old Equation | 3,13,000 + 20,000 | = | 3,03,000 + 30,000 | |

| Transactions | – 20000 + 0 | = | + 3000 + 20,000 | |

| N.E. | 2,93,000 + 20,000 | = | 3,03,000 + 10,000 | |

Explanation:- The transaction will affect both sides as cash has been paid so it is to be deducted from cash as well from creditors as payment made to them.

· Transaction related to Expenses

All the expense or Losses is to born by the owner although business has separate legal entity from its owner as He/She is the person who has taken risk to do business.

E. Rent paid Rs. 5,000.

Effect

| Assets | = | Capital + Liabilities | ||

| Cash Goods | Capital Creditors | |||

| Old Equation | 3,13,000 + 20,000 | = | 3,03,000 + 10,000 | |

| Transactions | – 5,000 + 0 | = | – 5000 + 0 | |

| N.E. | 2,88,000 + 20,000 | = | 2,98,000 + 10,000 | |

Explanation:- The transaction will affect both sides as cash has been paid so it is to be reduced as well as Capital is to be reduced because expense is to be born by the owner

· Transaction related to Income

Income or Profit is the reward for taking risk, as risk is taken by the owner so it is to be added in Capital.

F. Commission received Rs. 8,000.

Effect

| Assets | = | Capital + Liabilities | ||

| Cash Goods | Capital Creditors | |||

| Old Equation | 2,88,000 + 20,000 | = | 2,98,000 + 10,000 | |

| Transactions | + 8,000 + 0 | = | +8000 + 0 | |

| N.E. | 2,96,000 + 20,000 | = | 3,06,000 + 10,000 | |

Explanation:- The transaction will affect both sides as cash has been received so it is to be added back in cash as well as in Capital.

· Transaction related to Accrued/outstanding Income

Income is to be added back into the capital but as it is not received should be shown in the Assets Side as accrued Income because it meant to be received in this financial year.

A. Accrued Interest Rs. 10,000

Effect

| Assets | = | Capital + Liabilities | |

| Cash Goods Accured | Capital Creditors | ||

| Income | |||

| Old Equation | 2,88,000 + 20,000 + – | = | 3,06,000 + 10,000 |

| Transactions | + 8,000 + 0 + 10,000 | = | +10,000 + 0 |

| N.E. | 2,96,000 + 20,000 + 10,000 | = | 3,06,000 + 10,000 |

Explanation:- The transaction will effect both sides as Accrued Income has been added back to the capital & as it is not received so it is to be shown in the assets side as an asset.

· Transaction related to Prepaid or Advance Income

As Income received in advance so it is not belong to current financial year, so it cannot be added back to the Capital. It as an amount which is received by the business firm for the future course of activity till the activity not happened it is the Liability of the business.

| Assets | = | Capital + Liabilities | |

| Cash Goods Accured | Capital Creditors Prepaid | ||

| Income | Rent | ||

| Old Equation | 2,96,000 + 20,000 + 10,000 | = | 3,06,000 + 10,000 + |

| Transactions | + 5,000 + 0 + 0 | = | +10,000 + 0 + 5,000 |

| N.E. | 3,01,000 + 20,000 + 10,000 | = | 3,06,000 + 10,000 + 5,000 |

Explanation:-The transaction will effect both sides as Prepaid Income is a Liability should be shown in the Liability side & Cash received by the business should be added back to the Cash column of assets side.

2. Transaction affecting one side of the equation:

(I) Transaction affecting Assets side of the equation:

· Transaction related to Prepaid or Advance Expense

As Expense paid in advance so it is not belong to current financial year, so it can not be deducted from Capital. It as an amount which is paid by the business firm for the future course of activity till the activity not happened it is the Assets of the business.

A. Prepaid insurance paid Rs. 4,000

Effect

| Assets | = | Capital + Liabilities | |

| Cash Goods Accured Prepaid | Capital Creditors Prepaid | ||

| Income Expense | Rent | ||

| Old Equation | 3,01,000 + 20,000 + 10,000 – | = | 3,06,000 + 10,000 + 5,000 |

| Transactions | – 4,000 + 0 + 0 + 4,000 | = | + 0 + 0 + 0 |

| N.E. | 2,97,000 + 20,000 + 10,000 + 4,000 | = | 3,06,000 + 10,000 + 5,000 |

Explanation:- The transaction will affect both sides as Prepaid expense is a Asset should be shown in the Assets side & Cash paid by the business should be deducted from Cash column of assets side.

B. Purchased Machinery for Cash Rs. 80,000

Effect

| Assets | = | Capital + Liabilities | |

| Cash Goods Accured Prepaid Machinery | Capital Creditors Prepaid | ||

| Income Expense | Rent | ||

| Old Equation | 2,97,000 + 20,000 + 10,000 + 4,000 – | = | 3,06,000 + 10,000 + 5,000 |

| Transactions | – 80,000 + 0 + 0 + 0 80,000 | = | + 0 + 0 + 0 |

| N.E. | 2,17,000 + 20,000 + 10,000 + 4,000 80,000 | = | 3,06,000 + 10,000 + 5,000 |

Explanation:- The transaction will affect one side as cash has been paid for purchased of machinery & Machine is an fixed asset so it is separately shown in the asset side as well as cash is to be reduced.

(II) Transaction affecting Liability side of the equation:

· Transaction related to outstanding Expense

As Expense not paid yet or Outstanding but belong to current financial year so it is deducted from Capital & business has to pay it in near future so it is the liability of the firm.

A. Salary outstanding Rs. 8,000

Effect

| Assets | = | Capital + Liabilities | |

| Cash Goods Accured Prepaid Machinery | Capital Creditors Prepaid Outstanding | ||

| Income Expense | Rent Exp | ||

| Old Equation | 2,17,000 + 20,000 + 10,000 + 4,000 + 80,000 | = | 3,06,000 + 10,000 + 5,000 |

| Transactions | – 0 + 0 + 0 + 0 + 80,000 | = | – 8,000 + 0 + 0 + 8,000 |

| N.E. | 2,17,000 + 20,000 + 10,000 + 4,000 + 80,000 | = | 3,06,000 + 10,000 + 5,000 + 8,000 |

Explanation:- The transaction will affect Liability side as outstanding expense is a Liability should be shown in the Liability side & Expense should be deducted from Capital

· Transaction related to Interest on Capital

As interest on capital is the Expense of business it should be shown or deducted in the capital as well as interest of capital is the amount which is to be given to the owner as capital is the amount which is invested by the owner, therefore it is to be added back to Capital.

A. Interest on Capital Rs. 10,000

| Assets | = | Capital + Liabilities | |

| Cash Goods Accured Prepaid Machinery | Capital Creditors Prepaid Outstanding | ||

| Income Expense | Rent Exp | ||

| Old Equation | 2,17,000 + 20,000 + 10,000 + 4,000 + 80,000 | = | 3,06,000 + 10,000 + 5,000 + 8,000 |

| Transactions | – 0 + 0 + 0 + 0 + 0 | = | – 10,000 |

| + 10,000 + 0 + 0 + 0 | |||

| N.E. | 2,17,000 + 20,000 + 10,000 + 4,000 + 80,000 | = | 3,06,000 + 10,000 + 5,000 + 8,000 |

Explanation:-The transaction will affect Liability side as Interest of Capital should be added back & deducted from Capital as both of them belong to the owner.

· Transaction related to interest on Drawing

As interest on Drawing is the Income of business it should be shown or added back in the capital as well as interest of Drawing is the amount which is to be given by the owner to the business so it is treated as drawing and deducted from the Capital.

A. Interest on Drawing Rs. 1,000

Effect

| Assets | = | Capital + Liabilities | |

| Cash Goods Accured Prepaid Machinery | Capital Creditors Prepaid Outstanding | ||

| Income Expense | Rent Exp | ||

| Old Equation | 2,17,000 + 20,000 + 10,000 + 4,000 + 80,000 | = | 3,06,000 + 10,000 + 5,000 + 8,000 |

| Transactions | – 0 + 0 + 0 + 0 + 0 | = | – 1,000 |

| + 1,000 + 0 + 0 + 0 | |||

| N.E. | 2,17,000 + 20,000 + 10,000 + 4,000 + 80,000 | = | 3,06,000 + 10,000 + 5,000 + 8,000 |

Explanation:- The transaction will effect Liability side as Interest of Drawing should be added back & deducted from Capital as both of them belong to the owner.

· Transaction related to Drawing

As Drawing is the amount withdrawn by owner from business so it is to be deducted from Capital & also from the Cash.

A. Owner withdrew cash of Rs. 10,000

| Assets | = | Capital + Liabilities | |

| Cash Goods Accured Prepaid Machinery | Capital Creditors Prepaid Outstanding | ||

| Income Expense | Rent Exp | ||

| Old Equation | 2,17,000 + 20,000 + 10,000 + 4,000 + 80,000 | = | 3,06,000 + 10,000 + 5,000 + 8,000 |

| Transactions | – 10,000 + 0 + 0 + 0 + 0 | = | – 1,000 + 0 + 0 + 0 |

| N.E. | 2,17,000 + 20,000 + 10,000 + 4,000 + 80,000 | = | 3,06,000 + 10,000 + 5,000 + 8,000 |

Explanation:- The transaction will affect both sides as Drawing should be deducted from Capital & also deducted from Cash as withdraw by owner.

RULES OF DEBIT & CREDIT

Every business transaction affects two or more accounts. An account is summarised record of transaction at one place relating to a particular head. An account is divided into two parts i.e. debit Credit. Debit refer to the left side of an account and Credit refers to the right side of an account

Approaches for the rules of Debit & Credit

1. Traditional Approach

Under this approach, all ledger accounts are mainly classified into two categories:-

(I) Personal Accounts: It includes all those accounts which are related to any person i.e. Individuals, firms, companies, Banks etc. This can further classified into three categories:-

1. Natural Persons: All the accounts of human beings / Persons are included such Ram A/C, Shyam A/C etc.

2. Artificial Persons: This includes all such accounts which are treated as persons in the eyes of law & have separate legal entity such as Reliance Ltd., XYZ Ltd.

3. Representative Persons: This includes all such accounts which represents some persons such as Capital (Represent Owner) Outstanding Salary (Represent Employee)

(II) Impersonal Accounts: It includes all those accounts which are not related to any person this can be classified as :-

1. Real Accounts: Under this all accounts related to assets are included ( except Debtors). These can be Tangible i.e. Machinery, Furniture , Building, Cash etc. and Intangible I.e. Goodwill, Trade Mark, Patents Rights etc.

2. Nominal Accounts : this includes all the accounts related to Expenses/Losses & Incomes / Gains e.g. Salary, Rent, Commission received etc. they are used to record the transaction in the books of accounts.

Rules of Debit/Credit under Traditional Approach

| Classification of Accounts | Rules of Dr./ Cr. |

| Personal Accounts (All Personal Accounts) | Debit the receiver, Credit the Giver |

| Real Account | Debit what Comes In, Credit whats Goes Out |

| Nominal Account | Debit all Losses/Expenses, Credit all Income / Gains. |

SOURCE DOCUMENTS

A written document which provides evidence of the transactions is called the Source Documents. Source document is the first evidence of a transaction which takes place such as Cash Memo, Bill or Invoice, Receipt, Pay-in-slip, cheques, Debit-Note & Credit -Note.

(a) Invoice (Bill): An invoice is prepared by Seller at the time of sale of goods on credit. It contains details such as the goods sold, the party to whom goods are sold, sales amount, date etc.

(b) Cash Memo : It is prepared by the Seller at the time of Sale of goods on Cash. It contains details such as goods sold, quantity, amount received, date etc.

(c) Pay-in-Slip : It is used to deposit cash or cheque into bank. It has a counterfoil which is returned to the depositor with the Signature of the authorized person.

(d) Receipt: it is used when a customer give cash to the Business firm. It is an acknowledgement of payment or cash received by firm.

(e) Cheque : A cheque is a order in writing, drawn upon a specified banker and payable on demand.

(f) Debit Note : it is prepared when a buyer returned goods to seller or when purchased return transaction is entered in the books of accounts. It is prepared by the buyer of the goods.

(g) Credit Note : it is prepared when a seller received goods from buyer or when Sales return transaction is entered in the books of accounts. It is prepared by the Seller of the goods.

VOUCHER

A voucher is a document evidencing a business transaction. Recording in books of accounts are done on the basis of voucher. It is an accounting evidence of a business transaction.

Classification of Accounting Vouchers

| Vouchers | Further classification | Purpose |

| Cash Vouchers | Debit Vouchers

Credit Vouchers |

To show Cash Payment

To show Cash Receipt |

| Non Cash Voucher | Transfer Voucher | To show Transactions not involving cash |

CASH VOUCHERS

Cash voucher is prepared to record all the transactions which involve cash either in the form of receipt or payment. Thus cash voucher is further classified into Debit Voucher & Credit Voucher.

Format of Credit Voucher

| M/s Pratibha Furnitures

180, Nai Sarak, Delhi |

|

| Voucher No . ………………. Date………………. | |

| DEBIT …………………………………………………………………………………………….

………………………………………………………………………………………………………….. ………………………………………………………………………………………………………….. Total |

Amount (In Rs.) |

| Signature Manager Signature

Accountant |

|

Transfer Voucher/Non-Cash Voucher

This type of vouchers are prepared in those transactions which do not involve Cash. Such as Credit Sales, Credit Purchases, Bad Debts, Depreciation charged etc.

Transfer Voucher

| M/s Shyam Traders

156, Subhash Nagar, New Delhi |

|

| Voucher No . ………………. Date………………. | |

| DEBIT : -…………………………………………………………………………………………..

………………………………………………………………………………………………………….. ………………………………………………………………………………………………………….. Total |

Amount (In Rs.) |

| CREDIT : – ……………………………………………………………………………………….

………………………………………………………………………………………………………….. ………………………………………………………………………………………………………….. Total |

Amount (In Rs.) |

| Signature Manager Signature

Accountant |

|

JOURNAL

The first book in which the transactions of a business unit are recorded is called Journal. Here, business transactions are recorded in chronological order i.e. in the order in which they occur. Each record in a journal is called an entry. As a journal is the first book in which entries are recorded, it is also known as a book of original entry.

FORMAT OF JOURNAL

| Date | Particulars | L.F. | Amount (Rs.)

Dr. |

Amount (Rs.)

Cr. |

Ledger Folio (L.F.): Ledger Folio is the page No. of Ledger on which the Debit A/C & Credit A/C are to be posted.

TYPES OF ENTRIES

1. Simple Entry: It is that entry in which only two accounts are affected i.e. one account is debited and another account is credited with an equal amount.

2. Compound Entry : It is that entry in which more than two accounts are involved. Compound Entries can further be classified into single compound entry and double compound entry.

In Single Compound Entry several accounts are to be debited and only one account is to be credited or only one account is to be debited and several accounts are to be credited.

3. Opening Entry: The entry passed to record the closing balances of the previous year is called opening entry. While passing an opening entry, all assets accounts are debited and all liabilities accounts are credited.

Transaction related to Goods

| 1 | Goods purchased for cash

Purchase A/c Dr. To Cash A/c (Being goods purchased for cash) |

2 | Goods purchased from ram on Credit

Purchase A/c Dr. To Ram (Being goods purchased from Ram on credit) |

| 3 | Goods sold for cash

Cash A/C Dr. To Sales A/c (Being goods sold for cash) |

4 | Goods sold on credit to Mohan

Mohan Dr. To Sales A/c (Being goods sold to Mohan on credit) |

| 5 | Withdrawal of goods by owner for personal use

Drawings A/c Dr. To Purchase A/c (Being goods withdrew by owner for personal use) |

6 | Goods distributed as free samples

Advertisement A/c Dr. To Purchase A/c (Being goods distributed as free samples) |

| 7 | Goods given as charity

Charity A/c Dr. To Purchases A/c (Being goods given as charity) |

8 | Goods lost by fire/flood/theft etc.

Loss by fire/theft A/c Dr. To Purchase A/c (Being goods lost by fire/flood/theft) |

Note : Purchases A/c is credited in the above mentioned entries at S. No. 5 to 8 because the goods are going out of our business on cost and it is not a sale hence, deducted from the purchases A/c.

Transaction related to Bank

| 1 | Cash deposited into the bank

Bank A/c Dr. To Cash A/c (Being cash deposited to Bank) |

2 | Cash withdrawn for office use

Cash A/c Dr. To Bank A/c (Being cash withdrew from bank for office use) |

| 3 | When cheque is received from customer and deposited into bank same day.

Bank A/c Dr. To Customer’s personal A/c (Being cheques deposited into bank) |

4 | Cash withdrawn for personal use by owner.

Cash A/c Dr. To Bank A/c (Being cash withdrew for personal use) |

| 5 | When cheque is received from customer and not deposited into bank same day.

No Entry |

6 | When above cheque (Point 4) is deposited later into bank

Bank A/c Dr. To Customer s personal A/c (Being cheques deposited into bank received from …………….. On ………) |

| 7 | When payment is made through cheque

Personal A/c Dr. To Bank A/c (being payment made to …….. by cheque) |

8 | When expense is paid through cheque.

Expense A/c Dr. To Bank A/c (Being expense paid by cheque) |

| 9 | When interest is allowed by the bank.

Bank A/c Dr. To Interest A/c (Being interest allowed by bank) |

10 | When Bank charges for the services provided.

Bank Charges A/c Dr. To Bank A/c (Being Bank charges deducted) |

Note:- Bank A/C will be debited if the amount is deposited/credited by bank & Bank A/C will be credited if the amount is withdrawn/debited by bank.

Note:- Cash also will be debited if business receives it & Credited if Business paid it.

Transaction related to Expense or Income

| 1 | Expense paid by bank / Cash by the

Business Expense A/c Dr. To Cash / Bank A/c (Being expense paid by cash/Bank) |

2 | Expense is outstanding during a

Current F.Y. Expense A/c Dr. To Outstanding Exp. A/c (Being expense is due but not paid) |

| 3 | Expense paid in advance

Prepaid Expense A/c Dr. To Cash/Bank A/c (Being expense paid in advance by cash/ Bank) |

4 | Income received in Cash/Bank

Cash/Bank A/c Dr. To Income A/c (Being Income received in cash / bank) |

| 5 | Income due but not received

Outstanding Income A/c Dr. To Income A/c (Being Income due but not received) |

6 | Income received in cash/Bank in advance.

Cash/Bank A/c Dr. To Prepaid Income A/c (Being income received in advance) |

Transaction related to Expense or Income

| 1 | When Assets is purchased in Cash/Bank

Assets A/c Dr. To Cash / Bank A/c (Being Assets purchased in cash/Bank) |

2 | Depreciation charged on assets

Depreciation A/c Dr. To Assets A/c (Being Depreciation charged on assets @ …. %) |

| 3 | Assets Sold by the business

Cash/Bank A/C Dr. To Assets A/c (Being Assets sold in cash/Bank) |

4 | Liabilty arise when business raise funds.

Cash/Bank A/c Dr. To Liability A/c (Being fund raised) |

| 5 | Payment of Liability

Liability A/c Dr. To Cash/Bank A/c (Being Liability paid in Cash/Bank) |

Some other Journal Entries

| 1 | Bad Debts (when Debtors fail to pay due)

Bad Debts Dr. To Debtors A/c (Being amount Bad Debts ) |

2 | Bad Debts Recovered

Cash / Bank A/c Dr. To Bad Debts Recovered A/c (Being bad debts recovered ) |

| 3 | Debtors Become insolvent

Cash/Bank A/c Dr. (Amt. Received) Bad Debts Dr. (Amt. not rec.) To Debtors A/C (the due amt) (Being Debtors become insolvent could pay only …….. paise in a Rupees) |

4 | Interest on Capital

Interest on Capital A/c Dr. To Capital A/c (Being Interest on capital credited by business in capital A/c) |

| 5 | Interest on drawing

Capital A/C Dr. To Interest on Drawing A/c (Being interest on Drawing charged by business from capital A/c) |

Entries related to central sales Tax (CST)

| a | Central sales Tax (CST) collected on sales

Cash A/c Dr. To Sales A/c To Central sales tax A/c (Being Sales Tax deposited into Govt. A/c) |

b | When Central sales tax is deposited in Govt. A/c

Central sales tax A/c Dr. To Cash A/c (Being Sold goods & Sales Tax Collected) |

Journal Entries related to VAT (value added Tax),

| a | When VAT is paid on purchases sales

Purchases A/c Dr. VAT (Paid) A/c Dr. To Cash A/c Being goods purchase & VAT paid on purchase) |

b | When VAT is collected at the time of sales.

Cash A/c Dr. To Sales A/c To VAT (collected) A/c (Being Sold goods & VAT collected on sales) |

| c | When VAT is paid to the Government.

VAT (collected) A/c Dr. To VAT (Paid) A/c To Cash A/c (Being VAT paid to Govt.) |

Note:- In the last entry insurance paid for the whole year that why insurance for 11 month is treated as prepaid & insurance for the month of January is treated as expense.

BOOKS OF ORIGINAL ENTRY/SPECIAL PURPOSE BOOKS

As since the business grows and number of transactions increase, it becomes necessary for the necessary for the business to divide the recording work. The books maintained are illustrated below:

| Transactions | Further classification | Subsidiary Books Maintained |

| Cash & Bank Related Transactions | Only Cash

Cash & Bank Transactions Cash payment of small amount |

Simple Cash Book

Double Column Cash book Petty Cash Book |

| Transaction Other

than Cash & Bank |

Credit Sale

Credit Purchases Sales Returns/ Returns Inward Purchases Returns /Returns outward Any other transaction |

Sales Book

Purchases Book Sales returns Book Purchases Returns Book Journal Proper |

Advantages of Maintaining Subsidiary Books

· Division of work

· Leads to Specialization

· Easy to maintain Ledger

· Check on frauds

· Easy to fix responsibility

· Quick availability of required information.

Cash Book

Cash book shows all the transaction related to cash receipt and payments. Cash book serves two purpose. First, all the cash transactions are recorded first time in cash book it becomes Book of original entry. Second, there is no need to prepare Cash a/c in ledger it also play the role of Principal Book.

Simple Cash Book

All the cash receipts are shown in left hand side i.e. Debit side and all the cash payments are shown in right hand side i.e. Credit Side.

Points to Remember

· Cash in hand/opening balanced of cash is shown in Dr. side of the Cash book as “To Balance b/d”

· Only transaction of cash receipts and payments are recorded in this book.

· This book never shows a credit balance because one can’t pay more than the cash one have.

Notes: One can draw the following conclusions:

1. In a Simple Cash Book only cash receipts and cash payments are recorded. Credit transactions are not recorded. Purchases from Mohan of Rs. 5,000 on 15th Jan is a credit purchase hence, is not recorded in the Cash Book.

2. The debit side is always bigger than the credit side since the payments can never exceed the available cash. This is true even for daily balances.

3. It is like an ordinary account.

CASH BOOK WITH DISCOUNT COLUMN

Where cash discounts are allowed and received respectively, additional columns are provided on the debit side for discount allowed and on the credit side for discount received. The discount columns in the cash book are not parts of the cash book but are memoranda (provisional) columns because discount account is a nominal account while cash account is a real account. On balancing the cash book, the discount columns are singly totaled but not balanced.

CASH BOOK WITH DISCOUNT AND BANK COLUMN

In this case the Cash Book is ruled with there amount columns on either side of the cash book namely, “Discount, cash and Bank”. Cash columns in such a case will record actual cash received in the debit side and payments in the credit side. Cheques received should be entered on the debit side of the bank column when it deposited in the bank. The payments by cheques should be entered on the credit side in bank column and also when cash is withdrawn from the bank.

IMPORTANT ENTRIES

1. Contra Entries : These entries affect cash and bank columns both at the same time. To indicate contra entry “C” is mentioned in the L.F column of the cash Book. Following two cases result in Contra entries.

(2) Entries relating to cheques :

(a) When any payment is made by cheque : It will reduce the bank balance and thus bank column will be credited.

(b) When any payment is received in the form of cheque and no information about its deposit into bank is given. In this case it is assumed that the cheque is deposited into bank on the same day, when it is received & so bank A/c will be debited.

(c) When any payment is received in the form of cheque and it is deposited into bank on some other day i.e. when two dates, one for the receipt of cheque and the other for deposit. In this case no entry it to be recorded at the time of receiving the cheque. Entry is to made when cheque deposited in the bank, as bank column debited.

Petty Cash Book

Business has to incur small expenses which are repetitive in nature. To save the time and efforts of head cashier, business appoints a petty cashier. He is entrusted with the duty of paying these expenses.

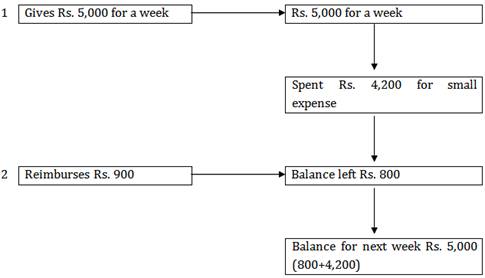

Imp rest System of Petty Cash Book

Under this system, Head cashier gives a fixed amount to petty cashier for a definite period. At the end of given period, Head cashier reimburses the amount actually spent by the petty cashier resulting the same amount with petty cashier which he had in the beginning of the period

This can be illustrated as under.

Head Cashier Petty Cashier

Advantage of Petty Cash Book

· Saving of time and efforts of Head cashier

· Control on Petty expenses.

· Less chances of fraud.

SPECIAL PURPOSE SUBSIDIARY BOOKS

Purchases Book

In this book, only those transactions are recorded which are related to credit purchases of goods in which the business deals in. Recording is made on the basis of Bills/ Invoices issued by the Suppliers.

Transactions not recorded in purchases Book

· Purchases of goods for cash.

· Purchases of Assets meant for long term, not for resale.

Note:-

1. Transaction of Aug. 5 is related to credit purchases of furniture i.e. an Asset.

2. On Aug. 17, goods bought for cash, Hence both the transaction are not recorded in Purchases Book.

Sales Books/Sales Journal

In this book, transactions for credit sales of goods are recorded. The source documents for this book is duplicate copy of invoice/bills issued to the customers.

Transactions not recorded in Sales Book

Sales of goods for cash

Sales of Assets.

Note:-

1. Transaction of Julyl5 is related to sale of asset,

2. Sale of Rama Furniture is made for cash, hence not recorded in Sales Book.

PURCHASES RETURNS/RETURNS OUTWARD BOOK

This book includes only those transactions which are related to returns of goods bought on credit. The goods may be returned due to various reasons such as goods bought being defective, supply of inferior quality goods etc. Entries in this book are made on the basis of Debit Note. A Debit note contains the name of the supplier to whom good are returned, details of goods returned

Sales Returns Book

This book includes all the returns by customers of credit sales of goods. The Credit Note is used The Credit Note is used for recording entries in this book. The credit note contains the details of customers and goods returned.

Recording of Transactions-I class 11 Notes

- CBSE Revision notes (PDF Download) Free

- CBSE Revision notes for Class 11 Accountancy PDF

- CBSE Revision notes Class 11 Accountancy – CBSE

- CBSE Revisions notes and Key Points Class 11 Accountancy

- Summary of the NCERT books all chapters in Accountancy class 11

- Short notes for CBSE class 11th Accountancy

- Key notes and chapter summary of Accountancy class 11

- Quick revision notes for CBSE exams

CBSE Class-11 Revision Notes and Key Points

Recording of Transactions-I class 11 Notes Accountancy. CBSE quick revision note for class-11 Mathematics, Physics, Chemistry, Biology and other subject are very helpful to revise the whole syllabus during exam days. The revision notes covers all important formulas and concepts given in the chapter. Even if you wish to have an overview of a chapter, quick revision notes are here to do if for you. These notes will certainly save your time during stressful exam days.

- Revision Notes for class-11 Physics

- Revision Notes for class-11 Chemistry

- Revision Notes for class-11 Mathematics

- Revision Notes for class-11 Biology

- Revision Notes for class-11 Accountancy

- Revision Notes for class-11 Economics

- Revision Notes for class-11 Business Studies

- Revision Notes for class-11 Computer Science

- Revision Notes for class-11 Informatics Practices

- Revision Notes for class-11 Geography

To download Recording of Transactions-I class 11 Notes, sample paper for class 11 Chemistry, Physics, Biology, History, Political Science, Economics, Geography, Computer Science, Home Science, Accountancy, Business Studies and Home Science; do check myCBSEguide app or website. myCBSEguide provides sample papers with solution, test papers for chapter-wise practice, NCERT solutions, NCERT Exemplar solutions, quick revision notes for ready reference, CBSE guess papers and CBSE important question papers. Sample Paper all are made available through the best app for CBSE students and myCBSEguide website.

- Introduction to Accounting class 11 Notes Accountancy

- Theory Base of Accounting class 11 Notes Accountancy

- Recording of Transactions-I class 11 Notes Accountancy

- Recording of Transactions-II class 11 Notes Accountancy

- Bank Reconciliation Statement class 11 Notes Accountancy

- Trial Balance and Rectification of Errors class 11 Notes Accountancy

- Depreciation, Provisions and Reserves class 11 Notes Accountancy

- Bill of Exchange class 11 Notes Accountancy

- Financial Statements – I class 11 Notes Accountancy

- Financial Statements – II class 11 Notes Accountancy

- Accounts from Incomplete Records class 11 Notes Accountancy

- Computerized Accounting System class 11 Notes Accountancy

Test Generator

Create question paper PDF and online tests with your own name & logo in minutes.

Create Now

Learn8 App

Practice unlimited questions for Entrance tests & government job exams at ₹99 only

Install Now