CBSE Accountancy Chapter 12 Computerized Accounting System class 11 Notes Accountancy in PDF are available for free download in myCBSEguide mobile app. The best app for CBSE students now provides Computerized Accounting System class 11 Notes Accountancy latest chapter wise notes for quick preparation of CBSE exams and school based annual examinations. Class 11 Accountancy notes on Chapter 12 Computerized Accounting System class 11 Notes Accountancy are also available for download in CBSE Guide website.

CBSE Guide Computerized Accounting System class 11 Notes

CBSE guide notes are the comprehensive notes which covers the latest syllabus of CBSE and NCERT. It includes all the topics given in NCERT class 11 Accountancy text book. Users can download CBSE guide quick revision notes from myCBSEguide mobile app and my CBSE guide website.

Computerized Accounting System class 11 Notes Accountancy

Download CBSE class 11th revision notes for Chapter 12 Computerized Accounting System class 11 Notes Accountancy in PDF format for free. Download revision notes for Computerized Accounting System class 11 Notes Accountancy and score high in exams. These are the Computerized Accounting System class 11 Notes Accountancy prepared by team of expert teachers. The revision notes help you revise the whole chapter in minutes. Revising notes in exam days is on of the best tips recommended by teachers during exam days.

Download Revision Notes as PDF

CHAPTER-12

COMPUTERS IN ACCOUNTING

Meaning of Computers: A computer is an electronic device, which is capable of performing a variety of operations as directed by a set of instructions. This set of instructions is called a computer programme.

Elements of Computer System:

A computer system is a combination of six elements:

1. Hardware

2. Software

3. People

4. Procedure

5. Data

6. Connectivity

1. Hardware: Hardware of computers consists of physical components such as keyboard, mouse, monitor, processor etc. These are electronic and electromechanical components.

2. Software: In order to solve a particular problem with the help of computers, a sequence of instructions written in proper language will have to be feed into the computers. A set of such instructions is called a ‘Program’ and the set of programs is called ‘Software’.

For example, a computer by feeding a particular software can be used to prepare pay-roll, whereas by feeding a second software it can be used to prepare accounts, by feeding a third software it can be used for inventory control and so on.

3. People: People are basically those individuals who use hardware and software to develop, maintain and use the information system residing in the computer memory. They constitute the most important part of the computer System. The main categories of people involved with the computer system are:

(a) System Analysis

(b) Operators

(c) Programmers

4. Procedures: The Procedure means a series of operations in a certain order or manner to achieve desired results. These are of three types:

(a) Software-Oriented: Provides a set of instructions required for using the software of a computer system.

(b) Hardware-Oriented: Provides details about the components and their methods of operations.

(c) Internal Procedure: Helps to ensure smooth flow of data to computers sequencing the operations of each sub-system of overall computer system.

5. Data: These are facts (may consist of numbers, text etc.) gathered and entered into a computer system. The computer system in turn stores, retrieves, classifies, organises and synthesis the data to produce information when desires.

Examples:

1. Bio-data of various applicants when the computer is used for recruitment of staff.

2. Marks obtained by various students in various subjects when the computer is used to prepare results,

6. Connectivity: the manner in which a particular computer system is connected to others (say through telephone lines, microwave transmission- satellite link etc.) is called element of connectivity.

Capabilities or Advantage of Computer System

A Computer system posses the following advantages in comparison of human beings:

1. High Speed: Computers are known for their lightening speed of operations and requires less time in comparison to human beings in performing a task. Most of modem computers perform millions of operations in one second.

2. Accuracy: Computers are extremely accurate. Their operations are error free and as such the information obtained from it is highly reliable. But sometimes errors occur due to bad programming or in accurate data feeding. In computer terminology, it refers is called Garbage in, garbage out (GIGO).

3. Reliability: Its reliability refers to the ability with which computer remains functional to serve the user. Unlike human beings these are immune to tiredness, boredom or fatigue, and can perform jobs of repetitive nature any number of times.

4. Versatility: It refers to the ability of computers to perform a variety of tasks. It can switch over from one programme to another. The same computer can be used for accounting work, stock control, sales analysis and even for playing games by the use of different softwares.

5. Storage: Memory or Storage capacity of a computer is so large that it can store any volume of information or data. Such data can be stored in it on magnetic discs, floppy discs, punched cards or microfilms etc. The information stored can be recalled at any time and also correction can be done within no time.

Limitations: Inspite of so many qualities, computers suffer from the following limitations.

(1) Lack of Common sense: Since computer work according to the stored programms, they simply lack of common sense.

(2) Zero I.Q.: Computers are dumb devices with zero Intelligence Quotient (IQ). They can’t visualize and think what exactly to do under a particular situation unless they are programmed to tackle that situation.

(3) Lack of Feeling: Computers lack feelings like human beings because they are machines. No computer passes the equivalent of a human heart and soul.

(4) Lack of Decision-making: Decision making is a complex process involving information, knowledge, intelligence, wisdom & ability to judge, Computers cannot make decisions of their own.

Some more limitations related to computerised System in Accounting

(1) High Cost of Training: Besides the high cost of computer system, huge money is required to get the trained specialised staff to ensure efficient and effective use of computerised systems.

(2) Danger of System Failure: The danger of system crashing due to hardware failure and the subsequent loss of word is a serious limitation of this system.

(3) Staff Opposition: Whenever the Accounting System is computerised, there is a significant degree of resistance from the existing staff because of the fear that they shall be less important to the organisation.

(4) Disruption: The accounting process suffer a significant loss of work and time when an organisation switches over to this system. This is due to the changes in the working environment that requires accounting staff to adapt to new system and procedures.

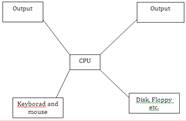

COMPONENTS OF COMPUTERS

The functional components consists of Input Unit, Central Processing Unit (CPU)and the out Unit relation as follows:

(1) Input Unit: It is for entering the data into the computer system. Keyboard and Mouse are the most commonly used input devices. Other such devices are magnetic tapes, disc, light pen, optical scanner, smart card reader etc. Besides there are some devices which respond to voice and physical touch.

(2) Central Processing Unit (CPU): It is the main part of computer hardware that actually processes the date according to the instructions it receives. It has three units:

Monitor Printer

(a)Arithmetic and Logic Unit (ALU): Responsible for performing all the arithmetic calculations such as addition, subtraction etc. and logical operations involving comparison among variables.

(b) Memory Unit: For storing the date.

(c) Control Unit: Responsible for controlling and coordinating the activities of all other units of the computer system.

(3) Output Unit: After processing the data, the information produced is. required in human readable and understandable form. Output devices perform this function. The commonly used devices are monitor, printer, graphic plotter (external) and magnetic stage devices (internal). A new device which is capable of producing verbal output that sound in human speech is also developed.

Operating Software

Operating Software is a set of programmes that is used by computers for various purposes. Operating Software is essential part of computer system in absence of operating software computer cannot operate. There are many operating soft- wares like Windows, Excel etc.

Utility Software

Utility Software is a set of computer programmes used to perform supporting operations in a computer. Utility Software are highly specialised and designed to perform only a single task or a small range of tasks.

Application Software

Application Software is the set of programmes which is designed and developed for performing certain task like accounting, word processing etc. for example Tally is the application software.

Accounting Information System (A1S)

Accounting Information System is a system of collecting, processing, summarising and reporting information about a business organisation in monetary terms. It maintains a detailed financial record of the business operations and transfer the data into valuable information.

So, Accounting Information System (AIS) is a sub-system of MIS. AIS is a struc- ture that allow its users to collect and use business data.

Application of Computers in Accounting

1. Recording of transactions: Record the all business transactions properly and timely.

2. Draw all ledger accounts: Computers prepares all ledger accounts by given transactions, like cash, bank, debtors, sales a/c etc.

3. Preparation of Trial Balance: It prepares the Trial Balance according to ledger accounts.

4. Preparation of Final A/c: It has utility to prepare Trading A/c, P&L A/c and Balance Sheet.

Features of Computerised Accounting System

Computerised accounting system is based on the concept of database. This system offers the following features:

(1) Online input and storage of accounting data.

(2) Printout of purchase and sales invoices.

(3) Every account and transaction is assigned a unique code.

(4) Grouping of accounts is done from the beginning.

(5) Instant reports for management, for example: Stock Statement, Trial Balance, Income Statement, Balance Sheet, Payroll Reports, Tax Reports etc.

Automation of Accounting Process

When accounting functions are done by computerised accounting software that is known as automation of accounting process under the automation of accounting process human activity is less but accounting software is more used.

So, accounting functions like posting into ledger, Balancing, Trial Balance and

Final Accounts are prepared by computer.

Stages of Automation

There are different stages of automation as:

(i) Planning: Under this stage the assessment of size, and business transactions is done for which automation has to be made.

(ii) Selection of Accounting Software: As there are many accounting softwares available in the market. So, in this stage appropriate accounting software is to be selected according to company’s need.

(iii) Selection of Accounting Hardware: Under this stage of automation the computer hardware is selected. This hardware should be such which can fullfill the accounting requirement and support the accounting software.

(iv) Chart of Accounts: Under this stage list of required heads of accounts is prepared.

(v) Grouping of Accounts: There are various transactions for Expenses, Income, Assets, Liabilities. All these transactions cannot be shown directly. So, these transactions are grouped as salary, wages, discount and commission etc.

(vi) Generation of Reports: This is final stage of automation under this final reports are prepared in from of Cash Book, Journal, Ledger, Trial Balance, P&L A/c and Balance Sheet etc.

Comparison of Manual and Compute red Accounting System

| Base | Manual Accounting | Computerised Accounting | |

| 1.

2. 3. 4. |

Identifying Financial Transactions

Recording Adjustment Financial statement |

In this system, it is done man ually according to principles.

In this system, entries are recorded man ually and other calculations also done manually. In this system, all adjustments entries are done manually. In this system, final statements is prepared manually |

In this system, it is also done manually according to principles.

In this, entries are recorded manually but other calculations are done by computers. In this system entries related to posting are done by computers. In this system final statement is prepared by computer with help of software. |

Sourcing of Accounting Software

India is one of software making country. So, accounting softwares are easily available in Indian Market. But it is more important to know what is your need of accounting software.

Generally, Tally accounting software is used in India which is easily available in market.

Accounting Softwares

(1) Readymade Software: Readymade Software are the software that are developed not for any specific user but for the users in general. Some of the readymade softwares available are Tally, Ex, Busy. Such softwares are economical and ready to use. Such softwares do not fulfill the requirement of very user.

(2) Customised Software: Customised software means modifying the readymade softwares to suit the specific requirements of the user Readymade softwares are modified according to the need of the business Cost of installation, main tenance and training is relatively higher than that of readymade user. There packages are used by those medium or large business enterprises in which financial transactions are some what peculiar in nature.

(3) Tailor-made Software: The softwares that are developed to meet the requirement of the user on the basis of discussion between the user and developers. Such softwares help in maintaining effective management information system. The cost of these softwares in very high and specific training for using these packages is also required.

Generic Considerations Before Sourcing Accounting Software

(i) Flexibility: a computer software system must be flexible in respect of data handling and report preparing.

(ii) Maintenance Cost: The accounting software must be such which has less maintenance cost.

(iii) Size of organisation: The accounting software must be according to need and size of organisation.

(iv) Easy to adaptation: The accounting software must be such which is easy to apply in organisation.

(v) Secrecy of data: The accounting software must be such which provide the secrecy of business data, from others.

Preparation of Accounts Groups

Groups of accounts means classifying the accounting transactions into different heads like Assets Group, Liabilities Group, Income Group and Expenses Group. By these grouping of accounts the final Accounts are meaningful for its users.

Generation of Accounting Reports

After collecting business data, it is converted into meaningful informations. Such summarised and converted information is known as a report.

The report is more effective if it is based on accurate and timely data.

A report must be relevant to users and contain all relevant information like Debtor’s Report, Creditor’s Report, Trial Balance and Financial Statement Report and others.

Scope

(i) The scope of the unit is to understand accounting as an information system for the generation of accounting information and preparation of accounting reports.

(ii) It is advised that the working knowledge of Tally software will be given to the students for generation of accounting software. For this, the teachers may refer chapter 4 of Class XII NCERT text book on Computerised Accounting System.

PROJECT

COMPREHENSIVE PROJECT

Mr. Deepak, after completing his graduation wants to start his own business but he was little bit confused which business to start. Moreover, he was short of funds also as only Rs.2,00,000 (to be used in business) were available with him, which he saved by doing part time jobs during his graduation. He discussed the matter with his father, Mr. Mahesh, a Bank Manager and decided to start a shop dealing in man’s wear from 1st April 2012 His father also help him in raising loan of Rs. 10,00,000 from xyz Bank against his personal guarantee. On 5th April 2012, Mr. Deepak open a Bank A/c with Rs. 5,000 in xyz Bank. Bank also credited his Bank A/c with the amount of loan on 1st June 2012, after completing all formalities, which is to be repaid in Ten equal yearly installments along with with interest @12% p.a. on 31st March every year. Same day he purchased a computer for Rs. 50,000 to maintain all the records regarding purchase, sales and stock and make the payment by cheque. He also deposited Rs. 45,000 in Bank.

It was also decided that all the purchases are to be made by cheques and all receipts on account of sales were to be deposited into Bank. He named his business as M/s Rajasthan Man’s wear and entered into a contract with a dis- tribute of Man’s wear on 15th June 2012. The distributer want him to make all the payments with regard to the orders in advance. Mr. Deepak’s transactions for the year ending on 31st March 2013 were as follows.

| Rs. | |

| Purchases (on 15 June 12) | 15,00,000 |

| Sales | 25,00,000 |

| Staff Salary | 2,00,000 |

| Telephone Expenses | 50,000 |

| Electricity charges | 1,00,000 |

| Packing charges | 25,000 |

| Insurance | 1,00,000 |

| Rent (Rs. 10,000 p.m.) | 1,20,000 |

| Carriage Inward. | 55,000 |

| Furniture purchased (on 1st June 12) | 1,00,000 |

25% payment for furniture was made by cash and rest by cheque. All the expenses were paid by cheque. Furniture and computer were depreciated @12% p.a. The closing stock on 31st Mar. 2013 was valued at Rs. 1,00,000. A plot/ land for Rs. 10,00,000 was also purchased on that day to construct shop in future. You are required to:

(1) Journalise the transactions.

(2) Post all the items to the relevant Ledger Accounts

(3) Prepare Trial Balance.

(4) Prepare Trading and Profit & Loss A/c and Balance sheet at the end of the year.

Journal

| Date | Particulars | L.F. | Dr. (Rs.) | Cr. (Rs.) |

| 2012

Apr 1 |

Cash A/c Dr.

To Capital A/c (Being business commenced) |

2,00,000 | 2,00,000 | |

| Apr 5 | Bank A/c Dr.

To Cash A/c (Being Bank A/c opened) |

5,000 | 5,000 | |

| June 1 | Bank A/c Dr.

To Bank Loan A/c (Being Bank Loan raised) |

10,00,000 | 10,00,000 | |

| June 1 | Computer A/c Dr.

To Bank A/c (Being Computer purchased) |

50,000 | 50,000 | |

| June 1 | Bank A/c Dr.

To Cash A/c (Being Cash deposit into Bank) |

45,000 | 45,000 | |

| June 1 | Furniture A/c Dr.

To Cash A/c To Bank A/c (Being furniture purchased & payment made in cash & by cheque) |

1,00,000 | 25,000

75,000 |

|

| June 15 | Purchase A/c Dr.

To Bank A/c (Being purchase made) |

15,00,000 | 15,00,000 | |

| Mar 31 | Bank A/c Dr.

To Sales A/c (Being Sales made) |

25,00,000 | 25,00,000 | |

| Mar 31 | Staff Salary A/c Dr.

To Bank A/c (Being Staff salary paid) |

2,00,000 | 2,00,000 | |

| Mar 31 | Telephone expenses A/c Dr.

To Bank A/c (Being Telephone exp paid) |

50,000 | 50,000 | |

| Mar 31 | Electricity Charges A/c Dr.

To Bank A/c (Being Electricity Charges paid) |

1,00,000 | 1,00,000 |

| Date | Particulars | L.F. | Dr. (Rs.) | Cr. (Rs.) |

| Mar 31 | Packing charges A/c Dr.

To Bank A/c (Being Packing charges paid) |

25,000 | 25,000 | |

| Mar 31 | Insurance A/c Dr.

To Bank A/c (Being Insurance paid) |

1,00,000 | 1,00,000 | |

| Mar 31 | Rent A/c Dr.

To Bank A/c (Being Rent paid) |

1,20,000 | 1,20,000 | |

| Mar 31 | Carriage Inward A/c Dr.

To Bank A/c (Being Carriage inward paid) |

55,000 | 55,000 | |

| Mar 31 | Bank Loan A/c Dr.

Interest on Loan A/c Dr. To Bank A/c (Being installment & interest loan paid) |

1,00,000

1,00,000 |

2,00,000 | |

| Mar 31 | Depreciation A/c Dr.

To Furniture A/c To Computer A/c (Being Electricity Charges paid) |

15000 | 10,000

5,000 |

|

| Mar 31 | Land A/c

To Bank A/c (Being plot land purchased) |

10,00,000 | 10,00,000 |

Capital Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Balance c/d | 2,00,000 | 1.4.12 | By Cash A/c | 2,00,000 | ||

| 2,00,000 | 2,00,000 | ||||||

| 1.4.12 | By Balance c/d | 2,00,000 |

Cash Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Capital c/d | 2,00,000 | 5.4.12 | By Bank A/c | 5,000 | ||

| 1.6.12 | By Bank A/c | 45,000 | |||||

| 1.6.12 | By Furnire A/c | 25,000 | |||||

| 2,00,000 | 2,00,000 | ||||||

| 1.4.13 | To Balance b/d | 1,25,000-> |

Bank Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 5.4.12 | To Cash A/c | 5,000 | 1.6.12 | By Computer A/c | 50,000 | ||

| 1.6.12 | To Bank Loan A/c | 10,00,000 | 1.6.12 | By Furniture A/c | 75,000 | ||

| 1.6.12 | To Cash A/c | 45,000 | 15.6.12 | By Purchase A/c | 15,00,000 | ||

| 31.3.13 | To Sale A/c | 25,00,000 | 31.3.13 | By Staff Salary A/c | 2,00,000 | ||

| 31.3.13 | By Telephone A/c | 50,000 | |||||

| 31.3.13 | By Electricity A/c | 1,00,000 | |||||

| 31.3.13 | By Packing Charges A/c | 25,000 | |||||

| 31.3.13 | By insurance | 1,00,000 | |||||

| 31.3.13 | By Rent A/c | 1,20,000 | |||||

| 31.3.13 | By Carriage A/c | 55,000 | |||||

| 31.3.13 | By Bank Loan A/c | 1,00,000 | |||||

| 31.3.13 | By Interest on Loan A/c | 1,00,000 | |||||

| 31.3.13 | By Land A/c | 10,00,000 | |||||

| 31.3.13 | By Balance c/d | 75,000 | |||||

| 35,50,000 | 35,50,000 | ||||||

| To Balance b/d | 75,000 |

Bank Loan Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Bank A/c | 1,00,000 | 1.6.12 | By Bank A/c | 10,00,000 | ||

| To Balance c/d | 9,00,000 | ||||||

| 10,00,000 | 10,00,000 | ||||||

| 1.4.13 | To Bal. b/d | 9,00,000 |

Purchases Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Bank A/c | 15,00,000 | 31.3.13 | By Bal. A/c | 15,00,000 | ||

| 15,00,000 | 15,00,000 | ||||||

| 1.4.13 | To Bal. b/d | 15,00,000 | 1.4.13 | To Bal. b/d |

Sales Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Bal. c/d | 25,00,000 | 31.3.13 | By Bank A/c | 25,00,000 | ||

| 25,00,000 | 25,00,000 | ||||||

| 1.4.13 | To Bal. b/d | 25,00,000 |

Computer Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 1.6.12 | To Bank A/c | 50,000 | 31.3.13 | By Dep. A/c | 5,000 | ||

| 50,000 | 31.3.13 | To Bal. b/d | 45,000 | ||||

| 1.4.13 | To Bal. b/d | 45,000 | 50,000 |

Furniture Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 1.6.12 | To Cash A/c | 25,000 | 31.3.13 | By Dep. A/c | 10,000 | ||

| 1.6.12 | To Bank A/c | 75,000 | 31.3.13 | To Bal. b/d | 90,000 | ||

| 1,00,000 | 1,00,000 | ||||||

| 1.4.13 | To Bal. b/d | 90,000 |

Staff Salary Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Bank A/c | 2,00,000 | 1.6.12 | By Bal. c/d | 2,00,000 | ||

| 2,00,000 | 2,00,000 | ||||||

| 1.4.13 | To Bal. b/d | 2,00,000 |

Telephone Expense Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Bank A/c | 50,000 | 31.3.13 | By Bal. c/d | 50,000 | ||

| 50,000 | 50,000 | ||||||

| 1.4.13 | To Bal. b/d | 50,000 |

Electricity Charges Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Bank A/c | 1,00,000 | 31.3.13 | By Bal. c/d | 1,00,000 | ||

| 1,00,000 | 1,00,000 | ||||||

| 1.4.13 | To Bal. b/d | 1,00,000 |

Packing Charges Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Bank A/c | 25,000 | 31.3.13 | By Bal. c/d | 25,000 | ||

| 25,000 | 25,000 | ||||||

| 1.4.13 | To Bal. b/d | 25,000 |

Insurance Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Bank A/c | 1,00,000 | 1.6.12 | By Computer A/c | 1,00,000 | ||

| 1,00,000 | 1,00,000 | ||||||

| 1.4.13 | To Bal. b/d | 1,00,000 |

Rent Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Bank A/c | 1,20,000 | 31.3.13 | By Computer A/c | 1,20,000 | ||

| 1,20,000 | 1,20,000 | ||||||

| 1.4.13 | To Bal. b/d | 1,20,000 |

Carriage Inward Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Bank A/c | 55,000 | 31.3.13 | By Bal. A/c | 55,000 | ||

| 55,000 | 55,000 | ||||||

| 1.4.13 | To Bal. b/d | 55,000 |

Interest Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Bank A/c | 1,00,000 | 31.3.13 | By Bal. A/c | 1,00,000 | ||

| 1,00,000 | 1,00,000 | ||||||

| 1.4.13 | To Bal. b/d | 1,00,000 |

Depreciation Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Furniture A/c | 10,000 | 31.3.13 | By Bal. c/d | 15,000 | ||

| To Computer A/c | 5,000 | ||||||

| 15,000 | 15,000 | ||||||

| 1.4.13 | To Bal. b/d | 15,000 |

Land Account

| Date | Particulars | J.F | (Rs.) | Date | Particulars | J.F. | (Rs.) |

| 31.3.13 | To Bank A/c | 10,00,000 | 31.3.13 | By Bal. A/c | 1,00,000 | ||

| 10,00,000 | 1,00,000 | ||||||

| 1.4.13 | To Bal. b/d | 10,00,000 |

Trial Balance as on 31.3.2013

| Particulars | Debit Balance | Credit Balance |

| Capital A/c

Cash A/c Bank A/c Bank Loan A/c Purchase A/c Sales A/c Computer A/c Furniture A/c Staff Salary A/c Telephone Expenses A/c Electricity Charges A/c Packing charges A/c Insurance A/c Rent A/c Carriage inward A/c Interest on Loan A/c Depreciation A/c Land A/c |

1,25,000

7,5000 15,00,000 45,000 90,000 2,00,000 50,000 1,00,000 25,000 1,00,000 1,20,000 55,000 1,00,000 15,000 10,00,000 |

2,00,000

9,00,000 25,00,000 |

| 36,00,000 | 36,00,000 |

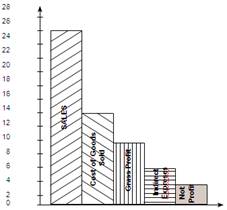

Trading & Profit & Loss A/c for the year ending on 31.3.2013

| Particulars | Rs. | Particulars | Rs. |

| To Purchases

To Carriage To Gross profit |

15,00,000

55,000 10,45,000 |

By Sales

By Closing stock |

25,00,000

1,00,000 |

| 26,00,000 | 26,00,000 | ||

| To Staff Salary

To Telephone Expenses To Electricity Charges To Packing Charges To Insurance To Rent To Interest on loan To Depreciation To Net Profit |

2,00,000

50,000 1,00,000 25,000 1,00,000 1,20,000 1,00,000 15,000 3,35,000 |

By Gross profit | 10,45,000 |

| 10,45,000 | 10,45,000 |

Trading & Profit & Loss A/c for the year ending on 31.3.2013

| Liabilities | Rs. | Assets | Rs. |

| Capital 2,00,000

Add: Net profit 3,35,000 Bank Loan |

5,35,000

9,00,000 |

Land

Furniture Computer Closing Stock Bank Cash |

10,00,000

90,000 45,000 1,00,000 75,000 1,25,000 |

| 14,35,000 | 14,35,000 |

Data relating to year 2012-13 of M/s Rajasthan Men’s wear

Cost of Goods sold = Opening Stock + Net Purchases + Direct Expenses – Closing stock

= 0 + 15,00,000 +55,000 – 1,00,000

= 14,55,000

OR

Cost of Goods Sold = Net Sales – Gross Profits

= 25,00,000 – 10,45,000

= 14,55,000

Computerized Accounting System class 11 Notes

- CBSE Revision notes (PDF Download) Free

- CBSE Revision notes for Class 11 Accountancy PDF

- CBSE Revision notes Class 11 Accountancy – CBSE

- CBSE Revisions notes and Key Points Class 11 Accountancy

- Summary of the NCERT books all chapters in Accountancy class 11

- Short notes for CBSE class 11th Accountancy

- Key notes and chapter summary of Accountancy class 11

- Quick revision notes for CBSE exams

CBSE Class-11 Revision Notes and Key Points

Computerized Accounting System class 11 Notes Accountancy. CBSE quick revision note for class-11 Mathematics, Physics, Chemistry, Biology and other subject are very helpful to revise the whole syllabus during exam days. The revision notes covers all important formulas and concepts given in the chapter. Even if you wish to have an overview of a chapter, quick revision notes are here to do if for you. These notes will certainly save your time during stressful exam days.

- Revision Notes for class-11 Physics

- Revision Notes for class-11 Chemistry

- Revision Notes for class-11 Mathematics

- Revision Notes for class-11 Biology

- Revision Notes for class-11 Accountancy

- Revision Notes for class-11 Economics

- Revision Notes for class-11 Business Studies

- Revision Notes for class-11 Computer Science

- Revision Notes for class-11 Informatics Practices

- Revision Notes for class-11 Geography

To download Computerized Accounting System class 11 Notes, sample paper for class 11 Chemistry, Physics, Biology, History, Political Science, Economics, Geography, Computer Science, Home Science, Accountancy, Business Studies and Home Science; do check myCBSEguide app or website. myCBSEguide provides sample papers with solution, test papers for chapter-wise practice, NCERT solutions, NCERT Exemplar solutions, quick revision notes for ready reference, CBSE guess papers and CBSE important question papers. Sample Paper all are made available through the best app for CBSE students and myCBSEguide website.

- Introduction to Accounting class 11 Notes Accountancy

- Theory Base of Accounting class 11 Notes Accountancy

- Recording of Transactions-I class 11 Notes Accountancy

- Recording of Transactions-II class 11 Notes Accountancy

- Bank Reconciliation Statement class 11 Notes Accountancy

- Trial Balance and Rectification of Errors class 11 Notes Accountancy

- Depreciation, Provisions and Reserves class 11 Notes Accountancy

- Bill of Exchange class 11 Notes Accountancy

- Financial Statements – I class 11 Notes Accountancy

- Financial Statements – II class 11 Notes Accountancy

- Accounts from Incomplete Records class 11 Notes Accountancy

- Computerized Accounting System class 11 Notes Accountancy

Test Generator

Create question paper PDF and online tests with your own name & logo in minutes.

Create Now

Learn8 App

Practice unlimited questions for Entrance tests & government job exams at ₹99 only

Install Now