CBSE class 12 Business Studies Controlling class 12 Notes Business Studies in PDF are available for free download in myCBSEguide mobile app. The best app for CBSE students now provides Controlling class 12 Notes Business Studies latest chapter wise notes for quick preparation of CBSE board exams and school based annual examinations. Class 12 Business Studies notes on chapter 8 Controlling are also available for download in CBSE Guide website.

CBSE Guide Controlling class 12 Notes Business Studies

CBSE guide notes are the comprehensive notes which covers the latest syllabus of CBSE and NCERT. It includes all the topics given in NCERT class 12 Business Studies text book. Users can download CBSE guide quick revision notes from myCBSEguide mobile app and my CBSE guide website.

12 Business Studies notes Chapter 8 Controlling

Download CBSE class 12th revision notes for chapter 8 Controlling in PDF format for free. Download revision notes for Controlling class 12 Notes and score high in exams. These are the Controlling class 12 Notes Business Studies prepared by team of expert teachers. The revision notes help you revise the whole chapter 8 in minutes. Revision notes in exam days is one of the best tips recommended by teachers during exam days.

Download Revision Notes as PDF

CBSE Class 12 Business Studies

Revision Notes

CHAPTER – 8

Controlling class 12 Notes Business Studies

Meaning & Definition: Controlling involves comparison of actual performance with the planned performance. If there is any difference or deviation, then finding the reasons for such difference and taking corrective measures or action to stop those reasons so that they don‘t re-occur in future and that organizational objectives are fulfilled efficiently.

Importance of Controlling

1. Controlling helps in achieving organizational goals: The controlling function measures progress towards the organizational goals and brings to light/indicates corrective action.

2. For Evaluating/Judging accuracy of standards: A good control system enables management to verify whether the standards set are accurate or not by careful check on the changes taking place in the organizational environment.

3. Making efficient use of resources: By the process of control, a manager seeks to reduce wastage of resources.

4. Improves employees motivation: A good control system ensures that employees know well in advance what they are expected to do & also the standard of performance. It thus motivates & helps them to give better performance.

5. Facilitating Coordination in action: In controlling each department and employee is governed by predetermined standards which are well coordinated with one another. Control provides unity of direction.

6. Ensuring order and discipline: Controlling creates an atmosphere of order and discipline in the organization by keeping a close check on the activities of its employees.

Nature of Controlling/Features of Controlling

1. Goal oriented: Controlling is directed towards accomplishment of organizational goals in the best possible manner.

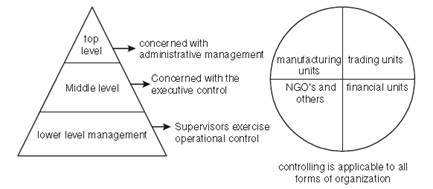

2. Pervasive: Controlling is an essential function of every manager and exercised at all levels of management.

3. Continuous: It is not an activity to be pursued in the end only; it has to be done on a continous basis.

4. Controlling is looking back: Controlling involves measurement of actual performance and its comparison with the desired performance. It is the process of checking and verification.

5. Controlling is forward looking: It is related to future because it seeks to improve future results on the basis of experience gained in the past.

6. Depends on planning: It pre supposes existence of planning because without planning no control is possible.

7. Action oriented*: Control has no meaning if no corrective action is taken; So timely action should be taken to prevent deviations.

8. Primary Function of Management* – controlling is performed at all levels and in all types of organizations.

9. Brings back management cycle back to planning:* Control should not be viewed as the last function. In fact it links back to planning. Controlling involves

• Comparing actual performance with standards • Finding out deviations • Taking corrective action so that they don‘t repeat in future These are the guidelines when future planning is done. Thus controlling not only completes one cycle of management process and also helps to improve planning in the next cycle.

Relationship between Planning and Controlling

Planning and controlling are interrelated and in fact reinforce each other in the sense that-

1. Planning is pre-requisite for controlling. Plans provide the standard for controlling. Thus, without planning, controlling is blind. If the standards are not set in advance managers have nothing to control.

2. Planning is meaningless without controlling. It is fruitful when control is exercised. It discovers deviations and initiates corrective measures.

3. Effectiveness of planning can be measured with the help of controlling.

4. Planning is looking ahead and controlling is looking back: Planning is a future oriented function as it involves looking in advance and making policies for the maximum utilization of resources in future that is why it is considered as forward looking function. In controlling we look back to the performance which is already achieved by the employees and compare it with plans. If there are deviations in actual and standard performance or output then controlling functions makes sure that in future actual performance matches with the planned performances. Therefore, controlling is also a forward looking function. Thus, planning & controlling cannot be separated. The two are supplementary function which support each other for successful execution of both the function. Planning makes controlling effective whereas controlling improves future planning.

Controlling Process

1. Setting Performance Standards: Standards are the criteria against which actual performance would be measured. Thus standards become basis for comparison and the manager insists on following of standards.

2. Measurement of Actual Performance: Performance should be measured in an objective and reliable manner which includes personal observation, sample checking. Performance should be measured in same terms in which standards have been established, this will facilitate comparison.

3. Comparing Actual Performance with Standard: This step involves comparison of actual performance with the standard. Such comparison will reveal the deviation between actual and desired performance. If the performance matches the standards it may be assumed that everything is under control.

4. Analysing Deviations: The deviations from the standards are assessed and analysed to identify the causes of deviations.

5. Taking Corrective Action: The final step in the controlling process is taking corrective action. No corrective action is required when the deviation are within the acceptable limits. But where significant deviations occur corrective action is taken.

Limitations of Controlling

1. Difficulty in setting quantitative standards:

Control system loses its effectiveness when standards of performance cannot be defined in quantitative terms. This makes comparison with standards a difficult task.

e.g areas like human behaviour, employee morale, job satisfaction cannot be measured quantitatively.

2. Little control on external factors:

An enterprise cannot control external factors like government policies, technological changes, competition. etc.

3. Resistance from employees:

Control is resisted by the employees as they feel that their freedom is restricted. E.g employees may resist and go against the use of cameras to observe them minutely.

4. Costly:

Control involves a lot of expenditure, time and effort. A small enterprise cannot afford to install an expensive control system.

Managers must ensure that the cost of installing and operating a control system should not exceed the benefits derived from it.

Controlling class 12 Notes Business Studies

- CBSE Revision notes (PDF Download) Free

- CBSE Revision notes for Class 12 Business Studies PDF

- CBSE Revision notes Class 12 Business Studies – CBSE

- CBSE Revisions notes and Key Points Class 12 Business Studies

- Summary of the NCERT books all chapters in Business Studies class 12

- Short notes for CBSE class 12th Business Studies

- Key notes and chapter summary of Business Studies class 12

- Quick revision notes for CBSE board exams

CBSE Class-12 Revision Notes and Key Points

Controlling class 12 Notes Business Studies. CBSE quick revision note for class-12 Business Studies, Chemistry, Math’s, Biology and other subject are very helpful to revise the whole syllabus during exam days. The revision notes covers all important formulas and concepts given in the chapter. Even if you wish to have an overview of a chapter, quick revision notes are here to do if for you. These notes will certainly save your time during stressful exam days.

- Revision Notes for class-12 Physics

- Revision Notes for class-12 Chemistry

- Revision Notes for class-12 Mathematics

- Revision Notes for class-12 Biology

- Revision Notes for class-12 Accountancy

- Revision Notes for class-12 Economics

- Revision Notes for class-12 Business Studies

- Revision Notes for class-12 Computer Science

- Revision Notes for class-12 Informatics Practices

- Revision Notes for class-12 English Core

- Revision Notes for class-12 History

- Revision Notes for class-12 Physical Education

To download Controlling class 12 Notes Business Studies, sample paper for class 12 Physics, Chemistry, Biology, History, Political Science, Economics, Geography, Computer Science, Home Science, Accountancy, Business Studies and Home Science; do check myCBSEguide app or website. myCBSEguide provides sample papers with solution, test papers for chapter-wise practice, NCERT solutions, NCERT Exemplar solutions, quick revision notes for ready reference, CBSE guess papers and CBSE important question papers. Sample Paper all are made available through the best app for CBSE students and myCBSEguide website.

- Nature and Significance of Management class 12 Notes Business Studies

- Principles of Management class 12 Notes Business Studies

- Business Environment class 12 Notes Business Studies

- Planning class 12 Notes Business Studies

- Organizing class 12 Notes Business Studies

- Staffing class 12 Notes Business Studies

- Directing class 12 Notes Business Studies

- Controlling class 12 Notes Business Studies

- Financial Management class 12 Notes Business Studies

- Financial Markets class 12 Notes Business Studies

- Marketing Management class 12 Notes Business Studies

- Consumer Protection class 12 Notes Business Studies

Test Generator

Create question paper PDF and online tests with your own name & logo in minutes.

Create Now

Learn8 App

Practice unlimited questions for Entrance tests & government job exams at ₹99 only

Install Now