CBSE Question Paper 2018 class 12 Economics (Reconducted) conducted by Central Board of Secondary Education, New Delhi in the month of March 2018. CBSE previous year question papers with solution are available in myCBSEguide mobile app and cbse guide website. The Best CBSE App for students and teachers is myCBSEguide which provides complete study material and practice papers to cbse schools in India and abroad.

CBSE Question Paper 2018 class 12 Economics (Reconducted)

Download as PDF

Class 12 Economics (Reconducted) list of chapters

Part-1

- Macro 01 Introduction

- Macro 02 National income accounting

- Macro 03 Money and Banking

- Macro 04 Income Determination

- Macro 05 The Government Budget and Economy

- Macro 06 Open Economy Macroeconomics

Part-2

- Micro 01 Introduction

- Micro 02 Theory of consumer behaviour

- Micro 03 Production and Costs

- Micro 04 Theory of the Firm Under Perfect Competition

- Micro 05 Market Equilibrium

- Micro 06 Non Competitive Markets

CBSE Question Paper 2018 class 12 Economics (Reconducted)

CBSE Question Paper 2018

Class 12 Economics (Reconducted)

Time allowed : 3 hours

Maximum Marks : 80

General Instructions:

- All questions in both the sections are compulsory.

- Marks for questions are indicated against each question.

- Question Nos. 1 – 4 and 13 – 16 are very short-answer questions carrying 1 mark each. They are required to be answered in one sentence each.

- Question Nos. 5 – 6 and 17 – 18 are short-answer questions carrying 3 marks each. Answers to them should normally not exceed 60 words each.

- Question Nos. 7 – 9 and 19 – 21 are also short-answer questions carrying 4 marks each. Answers to them should normally not exceed 70 words each.

- Question Nos. 10 – 12 and 22 – 24 are long-answer questions carrying 6 marks each. Answers to them should normally not exceed 100 words each.

- Answers should be brief and to the point and the above word limits should be adhered to as far as possible.

- Define opportunity cost.

Ans. The value of next best alternative foregone. - At what level of production is total cost equal to total fixed cost?

Ans. At zero level of output - Which of the following does not cause shift of supply curve of a good? (Choose the correct alternative)

- Price of input

- Price of the good

- Goods and services tax

- Subsidy

Ans. (b) Price of the good

- Which of the following measures of price elasticity shows elastic supply? (Choose the correct alternative)

- 0

- 0·5

- 1·0

- 1·5

Ans. (d) 1.5

- Explain the central problem of ‘‘What is produced and in what quantities’’.ORIn what circumstances may the production possibility frontier shift away from the origin? Explain.

Ans. This problem deals with the situation where an economy must decide as to what goods or services it must produce and in what quantity. It is because the resources are scarce/limited and can be put to alternative uses. (to be marked as a whole)ORProduction Possibility Frontier may shift away from origin, due to the following:

- Increase in resources

- Improvement in technologies

- A consumer buys 200 units of a good at a price of ₹20 per unit. Price elasticity of demand is (–) 2. At what price will he be willing to purchase 300 units? Calculate.

Ans.

New Price=Orignal Price(P)+20+(-)5=₹15 - Write a budget line equation of a consumer if the two goods purchased by the consumer, Good X and Good Y are priced at ₹ 10 and ₹ 5 respectively and the consumer’s income is ₹ 100.ORDefine marginal rate of substitution. Explain its behaviour along an indifference curve.

Ans. Budget Line equation:

m = PxQx + PyQy ; where m=income

Accordingly: 100 = 10Qx + 5QyORMarginal Rate of Substitution is defined as ‘the rate at which a consumer is willing to sacrifice units of a good to obtain one more unit of the other good.

Marginal Rate of Substitution diminishes as the consumer moves downward along the same indifference curve. It shows that consumer is willing to sacrifice lesser units of a Good Y, in order to gain one additional unit of Good X. This happens due to the operation of law of diminishing marginal utility. - Explain the conditions of producer’s equilibrium under perfect competition.

Ans. A producer is said to be in equilibrium when he produces that level of output at which :- MC = MR

- MC > MR after the MC = MR output level

Explanation to the conditions:

Condition – 1 MC=MR

Suppose when a producer starts producing a good, with the given factors and finds MR > MC he goes on producing because every new unit produced adds to profits.

As he goes on producing more units of the good he may face an output level when MC = MR and this output level satisfies MC = MR condition of equilibrium.

Condition – 2 MC>MR after the MC=MR output level

After MC = MR level, if MC > MR, every new unit produced is sold at a loss. So, he would not like to produce more units thereafter. Therefore, only that output level at which MC = MR, and beyond which MC > MR, is the output at which the producer is in equilibrium

- Explain the implications of ‘‘freedom of entry and exit of firms’’ under perfect competition.

Ans. ‘Freedom of Entry’, signifies that there are no barriers to the entry of new firms into industry. When the existing firms are earning supernormal profits, the new firms, attracted by the prospects of profit,enter the industry. This raises market supply which in turn leads tofall in market price and consequently profits. The entry continuestill each firm is earning just the normal profits.

‘Freedom to exit’, signifies that there are no barriers which restrictthe existing firms from leaving the industry. The firms try to leavewhen they are facing losses. As the firms start leaving market supply falls leading to rise in market price and consequently reduction in losses. The firms continue to leave till the losses are wiped out and each existing firm is earning just the normal profits. - A consumer consumes only two goods X and Y. Explain the conditions of consumer’s equilibrium using Utility Analysis.Ans. Assuming that a consumer is consuming only two goods X and Y, the conditions of consumer’s equilibrium (Utility Analysis) are:

- MU of a good as more unit of good are consumed.

Explanation

- Suppose The consumer will not be in equilibrium because per rupee MU of X is greater than per rupee MU of Y. This will induce the consumer to buy more of X by reducing expenditure on Y, leading to fall in MUx and rise in MUy. This will continue till the consumer attains the condition of

- Unless MU of a good falls, as more units are consumed the consumer will not reach the equilibrium.

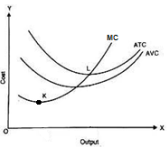

- Draw Average Variable Cost (AVC), Average Total Cost (ATC) and Marginal Cost (MC) curves in a single diagram. State the relation between MC curve and AVC & ATC curves.Ans. Examiners please check:

- MC curves intersects ATC and AVC curves at their minimum points.

- Vertical distance between ATC curve and AVC curve goes on declining as output increases.

Relationship among MC,AVC & AC :

When MC < ATC or AVC , ATC or AVC falls

MC = ATC or AVC , ATC or AVC constant

MC > ATC or AVC , ATC or AVC rises

- Define price floor. Explain the implications of price floor.ORMarket of a good is in equilibrium. If the demand for the good ‘decreases’. Explain the chain of effects of this change.

Ans. ‘Price Floor’ is the minimum price fixed by the government below which sellers cannot sell their product.

Since this price is normally set above the equilibrium price, there is excess supply in the market. As the seller may not be able to sell all that he wants to sell, he may illegally attempt to sell the product at a price below the floor price.ORMarket of a good is in equilibrium. If the demand for the good decreases this creates an excess supply of the good at the existing price, in the market.

– The excess supply creates competition among sellers, resulting in fall inprice, because sellers will not be able to sell all that they want to sell at the existing price.

– Fall in price leads to rise in demand and fall in supply.

– These changes continue till the market reaches new equilibrium. - Give one example of negative externalities.

Ans. Pollution created by factories/vehicles - Credit creation by commercial banks is determined by (Choose the correct alternative)

- Cash Reserve Ratio (CRR)

- Statutory Liquidity Ratio (SLR)

- Initial Deposits

- All the above

Ans. d) All of the above

- State the two components of M1 measure of Money Supply.

Ans. Currency held by public and demand deposits held by banks. - Define aggregate supply.

Ans. Aggregate Supply refers to the estimated money value of all the final goods and services planned to be produced in an economy. - Distinguish between stock and flow variables with suitable examples.ORWhat are capital goods? How are they different from consumption goods?

Ans. Any economic variable which is measured at a point of time is known as stock, e.g. capital,etc.

Whereas, any economic variable measured during a period of time is known as flow, e.g. income, etc. (any other relevant example)ORCapital goods are those durable goods which are used in production of goods and services,

Whereas consumption goods are those goods which are used for satisfaction of wants by the consumers. - Define investment multiplier. How is it related to marginal propensity to consume?

Ans. Investment Multiplier is a measure of the effect of change in initial investment on change in final national income.

There exist a direct relation between MPC and multiplier, i.e. higher the value of MPC, higher will be investment multiplier

- What is monetary policy ? State any three instruments of monetary policy.

Ans. Policy adopted by the Central Bank of an economy in the direction of credit control or money supply is known as Monetary Policy.

Instruments of Monetary Policy are Bank Rate, Repo Rate, Reverse Repo Rate, Cash Reserve Ratio. - Define full employment in an economy. Discuss the situation when aggregate demand is more than aggregate supply at full employment income level.OR What are two alternative ways of determining equilibrium level of income? How are these related?

Ans. Full Employment is a situation where those who are able and willing to work are getting work at the prevailing wage rate.

When Aggregate Demand is greater than Aggregate Supply at full employment, such a situation is known as Excess Demand or Inflationary Gap. It is called inflationary becausethis leads to a rise in general price level of the economy. (diagram not necessary)ORTwo alternative ways of determining equilibrium level of income are:

- Aggregate Demand – Aggregate Supply Approach (AD-AS Approach)

- Saving-Investment Approach (S-I Approach).

Interrelation between the two approaches:

AD=AS (AD-AS approach)

C+I = C+S

I=S (S-I approach)

These are first 20 questions only. To view and download complete question paper with solution

the best CBSE App from google playstore now or login to our Student Dashboard.

Economics (Reconducted) Question Paper 2018 with solution

Download class 12 Economics (Reconducted) question paper with solution from best CBSE App the myCBSEguide. CBSE class 12 Economics (Reconducted) question paper 2018 in PDF format with solution will help you to understand the latest question paper pattern and marking scheme of the CBSE board examination. You will get to know the difficulty level of the question paper. CBSE question papers 2018 for class 12 Economics (Reconducted) have 24 questions with solution.

CBSE Question Paper 2018

CBSE question papers 2018, 2017, 2016, 2015, 2014, 2013, 2012, 2011, 2010, 209, 2008, 2007, 2006, 2005 and so on for all the subjects are available under this download link. Practicing real question paper certainly helps students to get confidence and improve performance in weak areas.

- CBSE Question Papers for Class 12 Physics

- CBSE Question Papers for Class 12 Chemistry

- CBSE Question Papers for Class 12 Mathematics

- CBSE Question Papers for Class 12 Biology

- CBSE Question Papers for Class 12 Accountancy

- CBSE Question Papers for Class 12 Business Studies

- CBSE Question Papers for Class 12 Economics

- CBSE Question Papers for Class 12 History

- CBSE Question Papers for Class 12 Geography

- CBSE Question Papers for Class 12 Political Science

- CBSE Question Papers for Class 12 Physical Education

- CBSE Question Papers for Class 12 Computer Science

- CBSE Question Papers for Class 12 Informatics Practices

- CBSE Question Papers for Class 12 English Core

- CBSE Question Papers for Class 12 Hindi Core

- CBSE Question Papers for Class 12 Hindi Elective

- CBSE Question Papers for Class 12 Other Subjects

To download CBSE Question Paper 2018 class 12 Accountancy, Chemistry, Physics, History, Political Science, Economics, Geography, Computer Science, Home Science, Accountancy, Business Studies and Home Science; do check myCBSEguide app or website. myCBSEguide provides sample papers with solution, test papers for chapter-wise practice, NCERT solutions, NCERT Exemplar solutions, quick revision notes for ready reference, CBSE guess papers and CBSE important question papers. Sample Paper all are made available through the best app for CBSE students and myCBSEguide website.

Test Generator

Create question paper PDF and online tests with your own name & logo in minutes.

Create Now

Learn8 App

Practice unlimited questions for Entrance tests & government job exams at ₹99 only

Install Now